Equity loan, a financial tool often overlooked, holds the key to unlocking opportunities for homeowners and individuals seeking to leverage their property’s value. As we delve into the intricate world of equity loans, prepare to discover the ins and outs of this versatile lending option that can shape your financial future.

Introduction to Equity Loans

An equity loan, also known as a home equity loan, is a type of loan that allows homeowners to borrow money by using the equity in their property as collateral. This differs from other types of loans, such as personal loans or credit cards, as the equity in the home is used to secure the loan.

People might consider taking out an equity loan in situations where they need a large sum of money for a specific purpose, such as home renovations, debt consolidation, or education expenses. Since equity loans typically offer lower interest rates compared to other forms of credit, they can be an attractive option for those looking to access funds.

Benefits and Risks of Equity Loans

- Benefits: Equity loans often have lower interest rates, tax-deductible interest payments, and fixed monthly payments that make budgeting easier.

- Risks: The primary risk of an equity loan is the potential for foreclosure if the borrower fails to make payments, as the home is used as collateral.

Comparison of Equity Loans and Traditional Mortgage Loans

| Aspect | Equity Loan | Traditional Mortgage Loan |

|---|---|---|

| Interest Rates | Lower, fixed rates | Higher, potentially variable rates |

| Repayment Terms | Fixed monthly payments | Variable depending on the loan type |

| Eligibility Requirements | Based on equity in the home | Based on credit score, income, and debt-to-income ratio |

Calculating Available Equity for a Loan

To calculate the equity available for a loan, subtract the amount owed on the mortgage from the current market value of the property. For example, if a property is valued at $300,000 and has a mortgage balance of $200,000, the available equity would be $100,000.

A financial advisor may suggest considering factors such as the purpose of the loan, the ability to repay, and the potential impact on home equity before applying for an equity loan.

Types of Equity Loans

Equity loans come in different forms, each with its own unique features and benefits. Understanding the types of equity loans available can help you make an informed decision when considering borrowing against your home’s equity.

Home Equity Loans

Home equity loans allow homeowners to borrow a lump sum of money based on the equity they have in their property. These loans typically have fixed interest rates and fixed monthly payments over a set repayment term.

- Key Features: Fixed interest rates, lump sum payment, predictable monthly payments.

- Advantages: Predictable payments, ideal for one-time expenses.

- Disadvantages: Higher interest rates compared to HELOCs, limited flexibility.

The application process for a home equity loan involves submitting an application, providing documentation of income and property value, and undergoing a credit check.

Home equity loans are beneficial for homeowners who need a large sum of money for a specific purpose, such as home renovations or debt consolidation.

Home Equity Line of Credit (HELOC)

A HELOC is a revolving line of credit that allows homeowners to borrow against their home’s equity as needed. Borrowers can draw funds up to a certain limit and only pay interest on the amount borrowed.

- Key Features: Revolving credit line, variable interest rates, flexibility to borrow as needed.

- Advantages: Flexibility to borrow multiple times, lower initial interest rates compared to home equity loans.

- Disadvantages: Variable interest rates can increase over time, potential for higher total interest costs.

Applying for a HELOC involves a similar process to a home equity loan, including an application, documentation, and credit evaluation.

HELOCs are suitable for homeowners who anticipate ongoing expenses or want access to funds for emergencies or projects with variable costs.

| Loan Type | Interest Rates | Repayment Terms | Potential Risks |

|---|---|---|---|

| Home Equity Loan | Fixed | Fixed monthly payments over set term | Higher interest rates, limited flexibility |

| HELOC | Variable | Revolving credit line with interest-only payments initially | Variable rates, potential for increased interest costs |

Eligibility Criteria for Equity Loans

When applying for an equity loan, there are certain eligibility criteria that borrowers need to meet in order to qualify for the loan. Lenders consider various factors to assess the applicant’s ability to repay the loan and the risk involved. Here are some key points to understand about the eligibility criteria for equity loans:

Typical Eligibility Requirements

- Minimum credit score: Lenders typically require a minimum credit score of around 620 to qualify for an equity loan. A higher credit score can result in better loan terms.

- Stable income: Borrowers need to demonstrate a stable source of income to show their ability to repay the loan. Lenders may require income verification through pay stubs, tax returns, or bank statements.

- Low debt-to-income ratio: Lenders look at the borrower’s debt-to-income ratio to assess their ability to manage additional debt. A lower ratio increases the chances of loan approval.

- Equity in the property: Borrowers should have sufficient equity in their home, typically at least 15-20% equity, to qualify for an equity loan.

Factors Considered by Lenders

- Lenders consider the borrower’s credit history, income stability, employment status, debt obligations, and the value of the property when evaluating applicants for equity loans.

- Property appraisal and title search are also conducted to determine the property’s value and ownership status.

Tips to Improve Eligibility

- Improve credit score by paying bills on time, reducing debt, and correcting any errors on credit reports.

- Reduce existing debt to improve debt-to-income ratio and increase chances of loan approval.

- Maintain a stable source of income and provide necessary documentation to verify income.

Role of Credit Score and Income Verification

- Credit score plays a crucial role in the equity loan application process as it reflects the borrower’s creditworthiness and repayment history.

- Income verification helps lenders assess the borrower’s ability to repay the loan and determines the loan amount that can be approved.

Required Documents

- Documents needed for an equity loan application include proof of income, tax returns, bank statements, property information, and identification documents.

Acceptable Collateral Assets

- Acceptable assets that can be used as collateral for an equity loan include home equity, investment accounts, savings accounts, and valuable personal property.

Impact of Debt-to-Income Ratio

- Debt-to-income ratio is a key factor in qualifying for an equity loan, as it indicates the borrower’s ability to manage debt payments with their current income level. A lower ratio increases the likelihood of loan approval.

Applying for an Equity Loan

When you have decided to apply for an equity loan, it’s essential to understand the step-by-step process to ensure a smooth application experience. Let’s delve into the documentation required, common mistakes to avoid, evaluation criteria used by lenders, the significance of credit score, and a comparison table of interest rates and terms offered by different lenders.

Step-by-Step Process of Applying for an Equity Loan

- Research and compare lenders offering equity loans.

- Fill out the loan application form with accurate information.

- Submit the necessary documentation such as proof of income, property documents, and identification.

- Wait for the lender to evaluate your application.

- If approved, review the terms and conditions offered by the lender.

- Sign the loan agreement and receive the funds.

Documentation Needed to Apply for an Equity Loan

- Proof of income (pay stubs, tax returns).

- Property documents (deed of ownership).

- Identification (driver’s license, passport).

- Credit report and score.

- Bank statements.

Common Mistakes to Avoid During the Equity Loan Application Process

- Providing inaccurate information on the application form.

- Not reviewing the loan terms and conditions carefully.

- Missing or submitting incomplete documentation.

- Ignoring your credit score and how it affects your loan application.

Criteria Used by Lenders to Evaluate Equity Loan Applications

- Debt-to-income ratio.

- Loan-to-value ratio.

- Credit history and score.

- Income stability.

Importance of Credit Score in the Equity Loan Application Process

Maintaining a good credit score is crucial as it demonstrates your creditworthiness to lenders. A higher credit score can lead to better loan terms and lower interest rates.

Comparison Table of Interest Rates and Terms Offered by Different Lenders

| Lender | Interest Rate | Loan Term |

|---|---|---|

| Lender A | 3.5% | 10 years |

| Lender B | 4.0% | 15 years |

| Lender C | 3.25% | 20 years |

Sample Cover Letter:

[Your Name]

[Address]

[City, State, Zip Code]

[Email Address]

[Phone Number]

[Lender’s Name]

[Title]

[Lender’s Company]

[Company Address]

[City, State, Zip Code]Dear [Lender’s Name],

I am writing to submit my application for an equity loan with [Lender’s Company]. Attached, you will find all the required documentation, including proof of income, property documents, identification, and credit report.

I appreciate your time and consideration in reviewing my application. Please feel free to contact me if any additional information is needed.

Thank you for the opportunity.

Sincerely,

[Your Name]

Determining Loan Amount and Terms

When applying for an equity loan, it is crucial to understand how lenders calculate the loan amount and the factors that influence the terms of the loan. Negotiating favorable terms can significantly impact the overall cost and benefits of the loan.

Calculating Loan Amount

Lenders typically calculate the loan amount for an equity loan based on the value of the property and the amount of equity the borrower has. The most common method is the loan-to-value ratio, which is calculated by dividing the loan amount by the appraised value of the property. For example, if the appraised value of the property is $200,000 and the lender offers a loan-to-value ratio of 80%, the maximum loan amount would be $160,000.

Factors Influencing Loan Terms

Several factors influence the terms of an equity loan, including the borrower’s credit score, income, debt-to-income ratio, and the loan-to-value ratio. A higher credit score and lower debt-to-income ratio can lead to more favorable terms, such as lower interest rates and longer repayment periods. Additionally, a higher loan-to-value ratio may result in higher interest rates or additional fees to mitigate the lender’s risk.

Negotiating Favorable Terms

To negotiate favorable terms for an equity loan, borrowers can focus on improving their credit score, reducing their debt, and increasing the equity in their property. Shopping around and comparing offers from different lenders can also help borrowers find the best terms available. It is essential to review the terms carefully and consider the long-term implications before agreeing to any loan offer.

Repayment Options for Equity Loans

When it comes to repaying equity loans, borrowers have several options to consider in order to manage their debt effectively. Understanding the advantages and disadvantages of each repayment option is essential for making informed financial decisions.

Interest-Only Payments

One repayment option for equity loans is to make interest-only payments, where the borrower pays only the interest accrued on the loan each month. This can provide short-term relief by reducing monthly payments, but it may result in a larger overall cost of the loan since the principal balance remains untouched.

Extra Payments Towards Principal

Making extra payments towards the principal balance of an equity loan can help reduce the total interest paid over the life of the loan. By paying more than the minimum required amount each month, borrowers can shorten the repayment term and save on interest costs.

Choosing a Shorter Loan Term

In some scenarios, opting for a shorter loan term for repayment may be more beneficial than a longer term. While monthly payments may be higher, borrowers can save significantly on interest costs and become debt-free sooner.

Bi-Weekly Payments vs. Monthly Payments

Bi-weekly payments involve making half of the monthly mortgage payment every two weeks, resulting in an extra payment each year. This can help reduce the loan term and save on interest compared to monthly payments.

Refinancing for Favorable Terms

Refinancing an equity loan can allow borrowers to secure more favorable repayment terms, such as lower interest rates or shorter loan terms. This can help save money over time and improve overall financial stability.

Flexibility of HELOCs

Home equity lines of credit (HELOCs) offer greater flexibility in repayment compared to traditional equity loans. Borrowers can access funds as needed and only pay interest on the amount borrowed, providing a versatile financial tool for various needs.

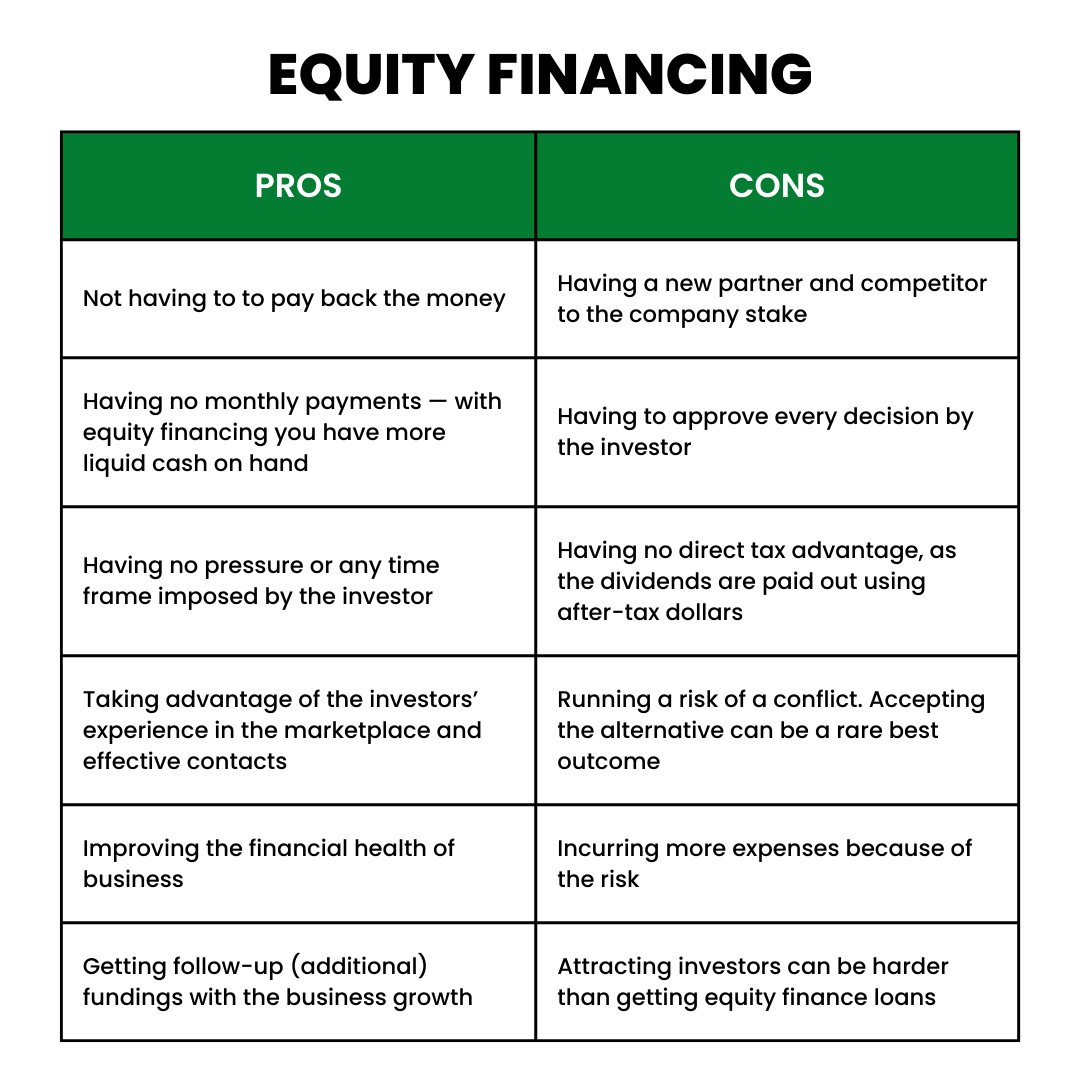

Benefits of Using Equity Loans

Using equity loans can offer several advantages for individuals looking to achieve their financial goals. These loans can be particularly helpful for purposes such as home improvements or debt consolidation. Here are some key benefits of using equity loans:

Financial Goals Achievement

- Equity loans provide access to a significant amount of funds, allowing individuals to undertake major financial projects such as home renovations or consolidating high-interest debts.

- By leveraging the equity in their property, borrowers can secure lower interest rates compared to other types of loans, resulting in potential savings over the loan term.

Successful Financial Strategies

- One successful financial strategy involving equity loans is using the funds to increase the value of the property through renovations, leading to potential appreciation in the property’s market value.

- Another strategy is using equity loans to pay off high-interest debts, consolidating them into a single loan with a lower interest rate, which can help individuals save on interest payments and simplify their debt management.

Comparison with Other Loans

- Equity loans differ from personal loans or credit cards in terms of interest rates and borrowing limits. Equity loans typically offer lower interest rates due to the collateral provided by the property, making them a cost-effective borrowing option.

- Unlike credit cards that carry high-interest rates, equity loans provide a lump sum of funds at a fixed interest rate, allowing borrowers to budget effectively and plan for repayments.

Risk Mitigation and Responsible Use

- While equity loans offer many benefits, there are risks involved, such as the potential loss of the property if the borrower fails to repay the loan. To mitigate this risk, borrowers should assess their repayment capacity and borrow responsibly within their means.

- It is essential to compare the interest rates and terms offered by different lenders for equity loans to secure the most favorable terms and ensure affordable repayments.

- To use equity loans responsibly, individuals should have a clear repayment plan in place, avoid borrowing more than necessary, and prioritize loan repayments to avoid financial pitfalls.

Risks and Considerations

Before taking out an equity loan, it is important to be aware of the potential risks involved and carefully consider various factors to make an informed decision.

Potential Risks of Equity Loans

- Interest Rates: Equity loans often come with variable interest rates, which can increase over time, leading to higher monthly payments.

- Foreclosure Risk: If you are unable to repay the loan, your home could be at risk of foreclosure as it serves as collateral for the loan.

- Decreased Equity: By taking out an equity loan, you are reducing the equity you have built up in your home, which could impact your financial stability in the long run.

Factors to Consider Before Taking an Equity Loan

- Financial Situation: Evaluate your current financial position and determine if you have the means to repay the loan in a timely manner.

- Loan Terms: Understand the terms of the loan, including interest rates, fees, and repayment schedule, to ensure they are favorable for your circumstances.

- Alternative Options: Explore other financing options that may be more suitable for your needs before committing to an equity loan.

Guidance for Mitigating Risks

- Shop Around: Compare offers from different lenders to find the most competitive rates and terms for your equity loan.

- Create a Repayment Plan: Develop a realistic repayment plan to ensure you can meet the monthly payments and avoid defaulting on the loan.

- Consult a Financial Advisor: Seek advice from a financial advisor to assess the impact of an equity loan on your overall financial plan and goals.

Impact of Equity Loans on Credit Score

When individuals take out an equity loan, it can have both positive and negative effects on their credit score. Understanding how equity loans impact credit scores is crucial for making informed financial decisions.

Strategies for Minimizing Negative Impacts on Credit Score

Taking specific measures can help minimize the negative impact of equity loans on credit scores. Some strategies include making timely payments, keeping credit card balances low, and avoiding taking on additional debt while repaying the equity loan.

Tips on Leveraging Equity Loans to Improve Creditworthiness

While equity loans can initially lower credit scores due to the new debt, consistently making on-time payments can demonstrate responsible financial behavior and ultimately improve creditworthiness over time. This can lead to a higher credit score in the long run.

Key Factors Influencing Credit Score with Equity Loans

| Factors | Impact on Credit Score |

|---|---|

| Payment history | Timely payments can positively impact credit score, while late payments can lower it. |

| Amount of debt | High levels of debt relative to available credit can negatively impact credit score. |

| Length of credit history | Longer credit history generally results in a higher credit score. |

| New credit | Opening new accounts, like an equity loan, can temporarily lower credit score. |

| Credit mix | Having a variety of credit types, including installment loans like equity loans, can positively impact credit score. |

An example scenario could involve an individual taking out an equity loan to consolidate high-interest debt. Initially, their credit score may drop due to the new loan, but if they make regular payments and reduce their overall debt, their credit score could improve over time.

Alternatives to Equity Loans

When considering financing options, there are alternatives to equity loans that individuals can explore. It is essential to weigh the pros and cons of each option carefully to determine the most suitable choice based on specific needs and circumstances.

Personal Loans

Personal loans are a common alternative to equity loans, offering a lump sum of money that can be used for various purposes. These loans typically have fixed interest rates and repayment terms, providing predictability for borrowers. However, personal loans may have higher interest rates compared to equity loans, making them more costly in the long run.

401(k) Loans

Borrowing from a 401(k) retirement account is another alternative to equity loans. This option allows individuals to access funds quickly without impacting their credit score. However, there are limitations on the amount that can be borrowed, and failure to repay the loan could result in penalties and tax consequences.

Credit Cards

Using credit cards for financing needs is a short-term alternative to equity loans. While convenient, credit cards often come with high-interest rates, making them an expensive borrowing option. It is essential to manage credit card debt carefully to avoid financial strain.

Home Equity Line of Credit (HELOC)

A HELOC allows homeowners to borrow against the equity in their property, similar to an equity loan. However, HELOCs offer more flexibility in borrowing and repayment, as funds can be accessed as needed. Interest rates on HELOCs may be variable, potentially leading to fluctuations in payments over time.

Tax Implications of Equity Loans

When it comes to equity loans, understanding the tax implications is crucial for maximizing benefits and avoiding potential pitfalls. One of the key advantages of equity loans is the potential tax benefits they offer, primarily in the form of tax-deductible interest.

Tax Deductible Interest

- Interest paid on a home equity loan may be tax-deductible, similar to mortgage interest, if the loan is used to improve the property securing the loan.

- Consult with a tax professional to determine eligibility for deducting interest on equity loans based on specific circumstances and intended use of funds.

- Keep detailed records of how the loan proceeds are used to ensure compliance with tax regulations and maximize deductions.

Variation in Tax Treatment

- The tax treatment of equity loans can vary depending on the purpose of the funds. For example, using the loan for home improvements may qualify for tax deductions, while using it for personal expenses may not.

- Understanding the specific tax rules and regulations related to equity loans is essential to make informed decisions and optimize tax advantages.

- Consider consulting with a tax advisor to navigate the complexities of tax implications associated with equity loans and ensure compliance with relevant laws.

Maximizing Tax Advantages

- Explore all possible tax deductions and credits associated with equity loans to maximize tax benefits while managing overall financial goals.

- Strategically plan the use of equity loan funds to align with tax regulations and optimize tax savings opportunities.

- Regularly review and adjust financial strategies in consultation with tax advisors to leverage tax advantages effectively and stay compliant with changing tax laws.

Case Studies and Examples

Real-life examples can provide valuable insights into the effective use of equity loans. Analyzing case studies can help us understand successful strategies as well as cautionary tales related to equity loan usage. Let’s explore some lessons learned from specific cases to assist readers in making informed decisions about equity loans.

Case Study 1: Successful Equity Loan Utilization

One family used an equity loan to renovate their home, increasing its value significantly. By investing in upgrades like a new kitchen, bathroom, and landscaping, they were able to sell their property at a higher price, covering the loan amount and making a profit. This case demonstrates how strategic use of equity loans can lead to financial gains.

Case Study 2: Cautionary Tale of Equity Loan Misuse

Another individual borrowed against their home equity to fund a luxurious vacation and unnecessary expenses. However, they underestimated the repayment terms and ended up struggling to make monthly payments, putting their home at risk of foreclosure. This case highlights the importance of careful planning and responsible borrowing when utilizing equity loans.

Future Trends in Equity Lending

As the financial landscape continues to evolve, the world of equity lending is also experiencing changes and advancements. It is crucial for borrowers to stay informed about the future trends in equity lending to make well-informed decisions regarding their financial needs.

Technology Integration in Equity Lending

With the rise of fintech companies and digital platforms, the process of applying for and managing equity loans is becoming more streamlined and efficient. Online applications, digital verification processes, and automated underwriting are some of the technological advancements shaping the equity loan landscape.

Regulatory Changes Impacting Equity Lending

Regulatory bodies are constantly updating and refining the rules governing equity lending to ensure consumer protection and financial stability. Changes in regulations regarding loan limits, interest rates, and borrower qualifications can have a significant impact on the availability and terms of equity loans.

Shift towards Personalized Loan Products

Financial institutions are increasingly offering personalized equity loan products tailored to the individual needs and preferences of borrowers. This trend allows borrowers to access loans with terms and features that align with their specific financial goals and circumstances.

Rise of Alternative Lenders in the Equity Market

Alternative lenders, such as online platforms and peer-to-peer lending networks, are gaining popularity in the equity lending space. These lenders often provide more flexible borrowing options and faster approval processes, challenging traditional banks and credit unions in the market.

End of Discussion

In conclusion, equity loans offer a myriad of possibilities for those looking to tap into their home’s equity for various financial needs. By understanding the nuances of equity loans and navigating the application process wisely, individuals can harness the full potential of this borrowing option to achieve their monetary goals with confidence.